1

Connect your channels in 15 minutes

Click to connect your ad platforms, analytics, and revenue sources. Secure ETL pipelines pull your data together automatically — no CSV uploads, no engineering tickets.

2

Models trained on your data, updated daily

Your brand's historical data trains models unique to your business — across channel, tactic, and campaign levels. Insights refresh daily, not quarterly.

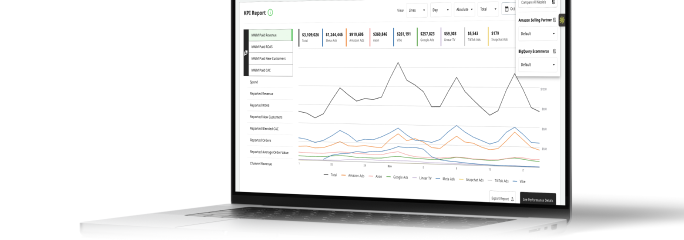

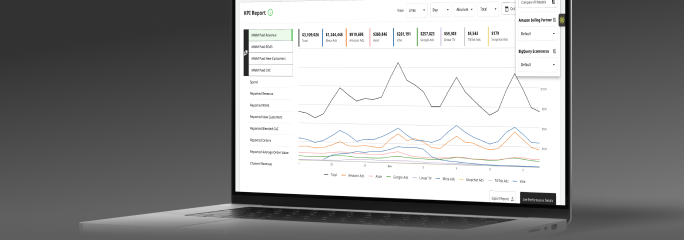

3

Forecast scenarios, optimize with confidence

Simulate budget changes across campaigns using saturation curves and confidence-backed forecasting. See the projected impact before you shift a dollar.